Market and Economic Conditions April 2020

/

Market and Economic Conditions April 2020

By Peter Klein, Chief Investment Officer/Founder, ALINEWEALTH

It was nearly a month ago when the stock markets in the US fell to multi-year lows – down 35%+ from the highs just made on February 19th. In less than 30 days the world changed dramatically. Most of the functioning economies globally have been shuttered while the global population is “sheltering in place”—unprecedented economic and societal conditions. What impact will these conditions have on the investment markets? On cash flows and earnings? Will once-vibrant industries and sectors remain solvent? How will consumers pivot to this new normal? How long will it take for global GDP to get back to trend line growth?

These and many other questions have been wracking the brains of many folks on Wall Street and the market environs around the world. However, despite these looming questions stock markets have leaped more than 25% since the lows last month. What do these investors see that most others do not? Or perhaps, said differently, what are these investors ignoring and by doing so are they putting their assets at irreparable risk?

What we do know, what is non-debatable, is that the global economy is functioning in an unprecedented “shuttered” space. Earnings for global companies of all stripes will be impacted and that we are in a global recession—the magnitude of which is still unknown. Likely takeaways from this massive stimulus are inflation and increased national debt levels, unemployment will be high, many business and sectors will not come back and, lastly, and most important to mindful investors, prices for mega-cap stocks have been inflated (big time) off the bottom via algorithmic trading and passive investing (both of which are indiscriminate buyers). These are knowns—what we do with this information (use it or ignore it) will be a determinant to long-term outcomes.

Let’s talk about that: decision making in the investment advisory world. You may know about several hedge fund managers who were quite vocal in the last 3 weeks about buying all sorts of stocks at what they deemed to be “generational low” prices. Shares that have been battered in sectors like airlines, travel, leisure and the like. While we respect their intestinal fortitude, their responsibilities are far different than ours. As a steward of other people’s capital—of their dreams, retirements, kids’ education—we must answer to a higher responsibility and in doing so cannot take undue risks, especially in times of crisis. From our lens, wealth management is less about being the “hot dot” or hitting home runs and more about maintaining a client’s overall risk and return mix—ensuring that long-term objectives are met.

A question that might come to mind is: How does an investment advisor determine what to do next in the portfolios under his stewardship? The answer from our vantage point is deep research, being open to new assumptions and robustly stress testing these scenarios. This is not a game folks—you just don’t throw a dart and buy the resulting stocks. Investing is a science and like any science doing one’s homework makes for good outcomes. I will leave the COVID-19 glide path to others infinitely more qualified to do so than I, but allow me, below, to focus on the science of finance.

The dispersion between the stock market indices that Wall Street popularizes and the ones they don’t is an important topic for investors. Many know that the Dow is made up of 30 stocks weighted through a factor devised decades ago. The S&P 500 is a much more diverse grouping but is weighted by market cap. So, the larger the stock’s market cap the more weight it carries. An extension of this cap weighting is the perverse nature of passive investing; the large-cap stocks must be purchased (indiscriminately) by index funds which in turn increases the value (through increased demand and a finite supply) of these stocks which in turn increases (faster and more significantly) the overall index levels. This set-up might sound like a self-fulfilling prophecy, one that has been powering the stock market for the last decade and one that can have a substantive impact if it were to unwind.

Exhibit A

Source: Factset

Looking at the chart above (Exhibit A) an investor (our “dart thrower”) might simply pick the growth indices and mimic them with a substantial majority of his invested capital (thus starting the aforementioned self-fulfilling prophecy) thinking that they offer the best opportunity for good outcomes going forward. Those last 2 words are most important: “going forward”. This action, of course, is a forecast – no investor knows what is going to occur (but as humans we prefer to the current state of things and what’s been working will continue to work). Let’s dig into what this passive investor is actually buying when they choose the “hot dot”.

The NASDAQ Composite index is home to companies—more than 30% of the index—that are unprofitable. That is, these companies do not generate any earnings. The Comp’s average PE (based on expected earnings for the next 12 months) is 26.2x and sports an average Price to Sales ratio of 3.7x and a Price to Book Value of 6.36x. The Comp’s dividend yield is 0.75% and has a (based on prior earnings) Return on Equity of 23.3%. But you may retort: “Who cares? It's going up!” This should be the cue for a good steward to say: “Yes, but the strategy may not be good for your long-term goals”. You see that’s the key to advice—providing it when it is uncomfortable and unpopular but always in the best long-term interests of the client.

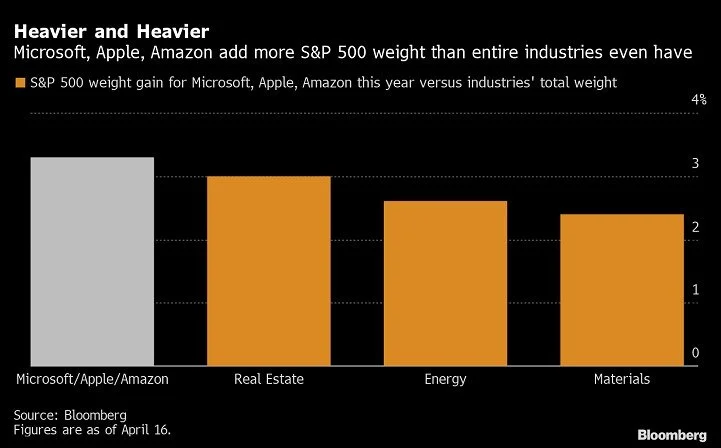

In other indices, there is also the concentration factor as the chart below (Exhibit B) shows. The IT sector representing more than 26% of the S&P’s total market cap (that’s 1 sector out of 11 that has a near 3x impact). And, as the next chart (Exhibit C) shows, if you look at just 3 of those stocks in the index, they are equal to the market cap of 3 entire sectors. While we can’t control fads in investing, we can choose to minimize their impact on the portfolio’s we manage.

Exhibit B

Exhibit C

So, what is an investor today to do? Develop a “Game Plan”—test your assumptions and re-test them and then have the patience and fortitude to act accordingly. This sounds simpler than it actually is and that is why the financial advisor profession exists—to ensure that clients stay on the optimal road to achieve their goals. Perhaps more importantly, to diffuse the emotionality of investing (especially in crisis periods) keep calm and stick to the plan. Of course, if the circumstances change then the Game Plan changes. But those circumstances are not day-to-day decisions (remember this pursuit is grounded science not speculating).

ALINE Wealth has developed a robust Game Plan which began several months ago when we argued that caution was warranted as we saw investors under-appreciating the risks. We wrote in these pages the importance of not chasing returns and earlier this year discussed the prospects of a “Minsky moment” (a condition popularized by economist Hyman Minsky) that stated a long period of complacency is replaced with spikes of volatility.

The ALINE Wealth Game Plan, well known by our clients, goes from a heavy allocation to “dry powder” to an action plan of allocating this dry powder to a series of well-researched investments when the markets provide an opportunistic opening (read: big down days when everyone else is selling). What gives us confidence that the market is just not going to go straight up? Well, there is the fact that we are in a global recession and that nations around the world have increased their overall debt levels substantially to help combat it. Not to mention that valuation levels are still quite robust. Finally, there is the historical context—the Bear market playbook–which calls for a re-test of the prior lows (as depicted on the chart below-Exhibit D).

Exhibit D

To ascertain the current state of the markets we also turn to that “exact science”—where emotions are held at bay and the figures rule—quantitative analysis. Looking at the estimate for S&P 500 operating earnings $174 as late as March 1 (let's call that “pre-COVID earnings estimates”). At the market’s high on February 19th, there were no deaths in the US (there was only one confirmed COVID death in the U.S. as of March 1st). Consensus expectations for 2020 are now in the $140 range (though there are some estimating as low as $100-110) and using a typical multiple of 16 we get an S&P target of 2240 (27% below where we are today). The S&P at 2850 is estimating a multiple close to 21x—far from the typical bear market recovery multiple of 10-11x. Let’s say earnings recover quickly (the oft-quoted “V-shape”) and at generous (given where we are macro-economically) multiple of 15.5 the current level on the S&P is targeting nearly $190 in earnings (about 10% ABOVE the pre-CV forecast in January).

Nevertheless Mr. Market and his disciples could apply a bullish multiple to these forward earnings expectations. This is what has apparently been the modus operandi for the market in the last 3 weeks. Color us skeptical.

The final piece of ALINE Wealth’s Game Plan is “proactive empathy”—our culture of reaching out to our clients—to review their portfolios, to stress test their comprehensive wealth management plan and to simply be there for them.

These are trying times folks. Please stay safe & healthy—both biologically and financially. We remain confident in the exceptionalism that has always been America and therefore this challenge—our generation’s test—will yet again show the world what is to be American.

ALINE Wealth is a group of investment professionals registered with HighTower Securities, LLC, member FINRA and SIPC, and with HighTower Advisors, LLC, a registered investment advisor with the SEC. Securities are offered through HighTower Securities, LLC; advisory services are offered through HighTower Advisors, LLC.